- Contactless Payment Turf Wars: Transit Platforms

- >Contactless Payment Turf Wars: PiTaPa Pitfalls

- Contactless Payment Turf Wars: Why Oyster is missing from mobile

- Contactless Payment Turf Wars: Tapping the potential of TAP

- Contactless Payment Turf Wars: Apple Card and the Prepaid Innovation of Apple Pay Suica

- Contactless Payment Turf Wars: EMV closed loop transit dumb cards

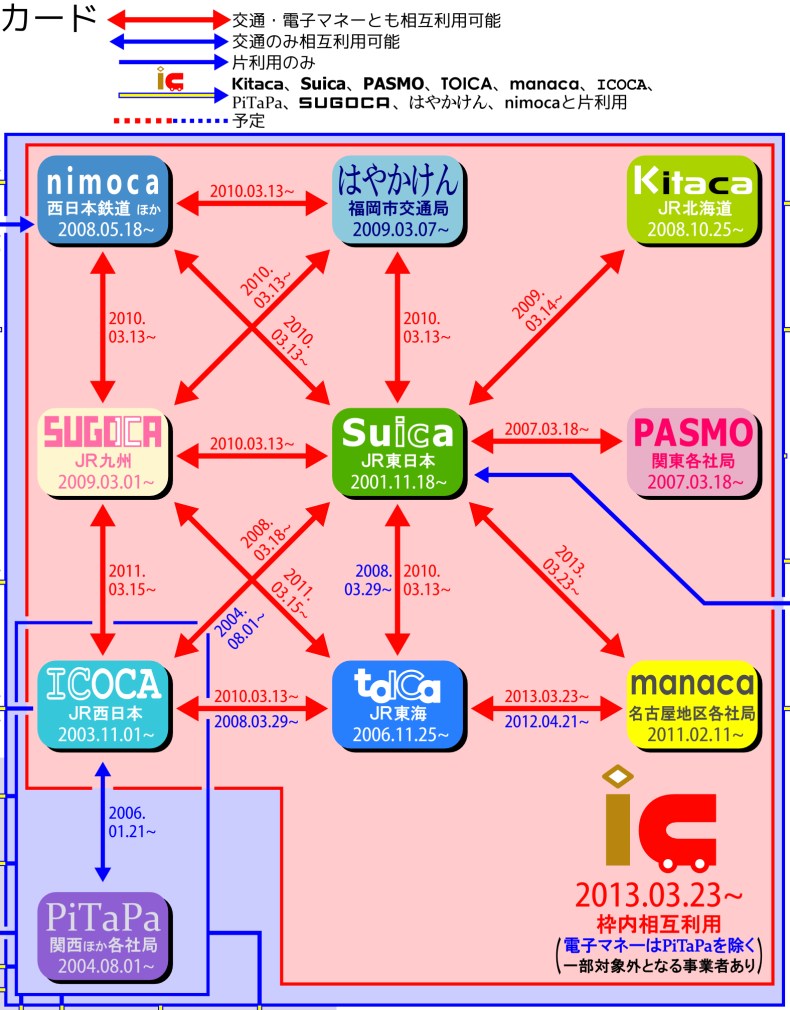

PiTaPa is the perpetual outliner of the major Japanese transit smartcards: Suica, ICOCA, TOICA, SUGOCA, Kitaca, PASMO, manaca, Nimoca, Hayaken. Starting in 2006 the major transit cards were stitched together into one common national platform for mutual transit and e-money use achieved by 2013. The result is the fertile ground that Apple Pay Suica is growing and thriving in. Apple Pay VP Jennifer Bailey recently said that Apple Pay is doing well in Japan. The Apple Pay Japan story is all Suica and transit reamains the golden uptake path for contactless payments on smarphones.

And then there is PiTaPa. PiTaPa is the main transit smartcard for non-JR ‘private’ rail companies in the Kansai: Hankyu, Keihan, Nankai and Hanshin. The excellent Japanese Transit IC map graphic on Wikipedia perfectly captures the problem of PiTaPa incompatibility and isolation: the background blue is transit only compatibility, the red is transit and e-money compatibility.

The PiTaPa Story

PiTaPa has an interesting history but not a particularly happy or successful one. It’s the perfect case study of what happens when banks and credit card companies call the shots on transit ticketing system infrastructure instead of letting transit company management make those decisions. It’s also a story of how most Japanese transit companies, except for JR East, failed to see the coming revolution of mobile digital wallet platforms.

The PiTiPa founding members originally planned to build a transit IC smartcard system just like Suica: pre-paid stored value (SV). Then Sumitomo Mitsu stepped in with a seemingly good idea: a Sumitomo Mitsui credit card + transit card post-pay combo card to save transit users from having to recharge the transit card smartcard at all. A credit card transit card for transit and shopping. What could go wrong? The Kansai area is home town for Sumitomo Mitsu, the Kansai banking indsutry Godzilla for over a hundred years, how could transit companies, Sumitomo Mitsu borrowers all, resist?

And so PiTaPa was born in 2004 as a Frankenstein credit card grafted with a transit card appendage that was supposed to do it all, but never delivered the benefits of either one. Sumitomo Mitsui imposed all the hoary old credit card conventions on the shiny new creation: credit checks and spending caps. It immediately shrunk the PiTaPa user base from everybody to people with good credit ratings who passed Sumitomo Mitsui credit checks. Compare this to Suica where everybody from kids to retirees with a ¥1,000 bill can buy Suica card at a station kiosk. That’s the beauty of stored value cards, simple immediate purchase and use.

The original PiTaPa did not sit well with a lot of transit users so a ‘PiTaPa lite’ card with deposits instead of credit checks, without the e-money function, was added in 2007. Unfortunately since PiTaPa was post-pay, PiTaPa didn’t work with the Japanese Transit IC e-money standard and was shunned by payment networks and merchants. Good luck trying to use PiTaPa credit outside of its core transit ghetto at 7 Eleven, other convenience stores or anywhere else.

If you want to know how well PiTaPa is doing in 2018 all you need to do is check the commuter pass pages of the PiTaPa member railroads: Keihan and Osaka Metro offer ICOCA commuter passes. Not only that but Osaka Metro and Keihan have moved away from PiTaPa commuter passes for general issue and use ICOCA instead.

{kind=link}

No Future

The decision to let Sumitomo Mitsui call the shots instead of transit management killed any viable future for the PiTaPa system. PiTaPa uses the same FeliCa technology behind the highly successful Mobile Suica and Apple Pay Suica, but the unique one-off system architecture, limited user base and transaction volume mean PiTaPa will never be hosted on any mobile digital wallet platform. PiTaPa transit partners don’t want to spend resources to build a cloud and host mobile service because there is too much cost for such little return. And Sumitomo Mitsu will certainly never foot the bill to clean up the mess they created.

Now that JR East and Sony have announced ‘Super Suica’ for April 2018 that will incorporate all Japan Transit cards into one card system for transit, e-money and mobile, the PiTaPa participants face a choice: junk the old PiTaPa and get onboard the Super Suica express or be left behind in isolation with no future.

Transit payment platforms

The basic unsolvable problem is that banks and credit card companies want different things than transit companies. Banks and credit card companies want credit checks and caps, transit companies need as many people going through the transit gate as efficiently and safely as possible. These fundamental business differences will never be resolved, there will always be tension. That is why banks and credit card companies should never be in charge of running transit gates. They simply want to take their credit card cut and run, leaving the scene of crime, and the cleanup bill, to others.

You can see the similar things playing out on other transit systems such as Hong Kong’s Octopus system with AliPay and other QR Code ‘virtual banks’ putting pressure on operators to change transit ticketing system infrastructure to suit their needs, all paid by the transit operator of course.

It’s wasteful nonsense and who needs it? It’s last century credit card vs. smartcard, open loop vs. closed loop thinking. Digital wallet platforms like Apple Pay and Google Pay conveniently collapse the differences of open loop vs. closed loop rendering the whole argument pointless while offering a whole new game. Build a transit payment platform instead, in the long run it’s a win-win for transit companies and the banking industry.

It’s very simple: transit companies and a finance industry that stick with the old ways of thinking will miss the major unique new business opportunities offered by transit payment platforms hosted on digital wallet platforms, opportunities that build on transit but also extend it to exciting new places, a transit platform that grows and benefits everyone.

You must be logged in to post a comment.